The Chokepoint in Global Supply Chains that No One Cares About

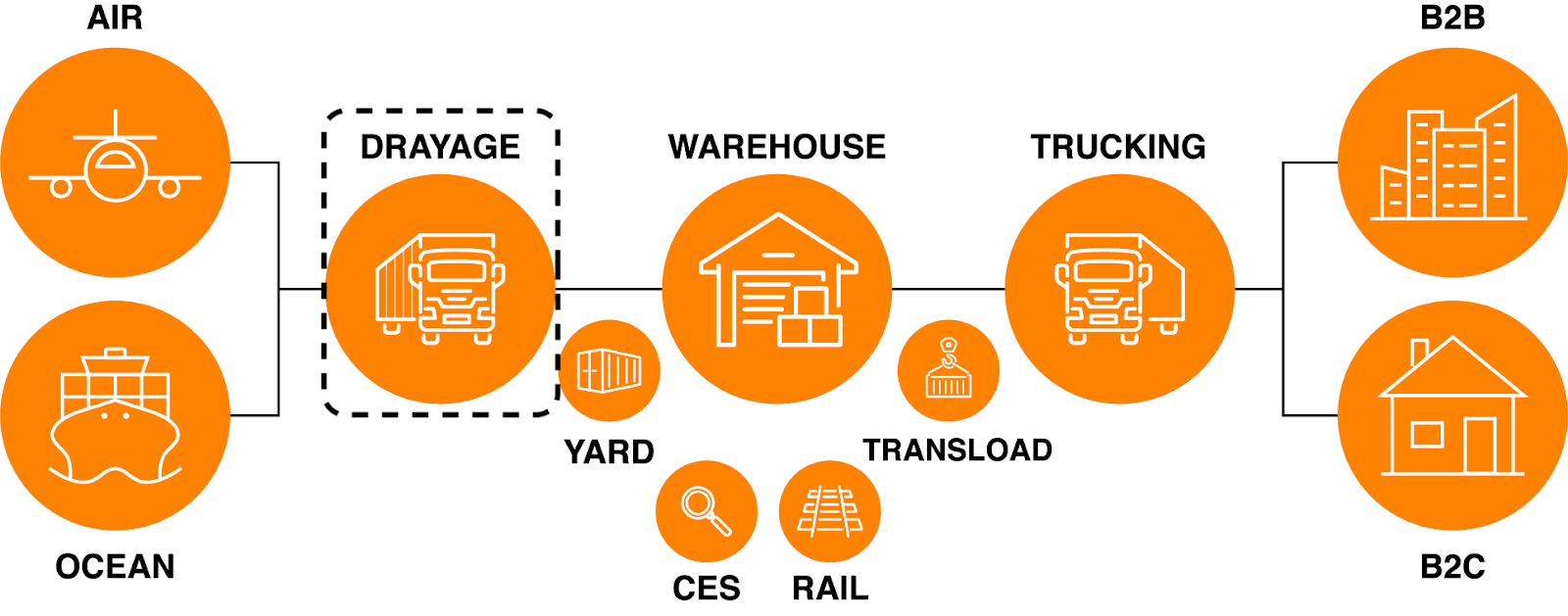

Drayage is a bit like the unsexy sidekick of logistics – short-haul truck moves, usually under 50 miles, shuttling containers between ports, rail yards, and nearby warehouses. But it’s also the linchpin of global trade, the critical handoff where ocean and rail cargo meet inland supply chains. When drayage stumbles, the ripple effects are brutal: delayed rail schedules, empty retail shelves, and frustrated shippers.

Unfortunately, according to most market estimates, the market size is relatively small from a tech investor POV ($27B in 2024, and projected to grow to $30B by 2030). Perhaps unsurprisingly then, there hasn’t been a lot of tech innovation within the drayage market over the years – certainly not like there has been in other parts of the logistics world. Dan Kopp, former CEO of ITG Transportation Services, tells me that “with many carriers lacking back-office support, let alone surplus cash to invest in tech, many of the operational aspects of drayage remain manual processes.” This tension is exactly what makes the space both frustrating and compelling: there aren’t a lot of dollars available (relative to other markets in logistics), but because it’s such a chokepoint to the rest of global trade, it could be a powerful wedge into much larger opportunities across the supply chain.

The Drayage Ecosystem

Every container hitting a North American port needs a drayage move. It’s non-negotiable. Yet, despite its importance, the sector is a mess of inefficiencies. Over 80% of drayage capacity comes from small owner-operators, often running one-truck operations with zero back-office support. This means they’re juggling port schedules, chassis shortages, and customer demands using Gmail, Google Maps, and whatever calculator app comes on their phone.

Some PE roll-ups now exist such (e.g., U.S. Multimodal Group (USMMG and Cargomatic), but few are true tech plays. Adoption challenges persist due to old-school operators and decentralized agency models (e.g., The Evans Network, US 1 Industries and ContainerPort Group).

New tech often hits a ceiling unless it's embraced by the fragmented agent networks and drivers. As such, tech expectations have remained very low in the drayage world – things like cloud-based ops or online pricing are still novel.

Drayage vs. Freight Forwarding: A Quick Breakdown

To understand drayage’s unique pain points, let’s contrast it with freight forwarding, which I’ve previously written about here:

Distance and Scope: Drayage is hyper-local – 50-100 miles, focused on quick port-to-warehouse turnarounds. Freight forwarding, by contrast, orchestrates global, multi-modal journeys spanning thousands of miles, often including drayage as a small piece.

Operational Focus: Drayage drivers wrestle with port chaos: terminal appointments, container storage, and chassis management. Freight forwarders deal with paperwork (bills of lading, customs forms) and coordinating handoffs, rarely touching the trucks themselves.

Pricing: Drayage is commoditized, with stable, predictable rates often listed on spreadsheets. Freight forwarding pricing is a complex puzzle, blending ocean, air, and drayage costs, with forwarders often hunting for the cheapest drayage bid to keep margins tight.

Fragmentation: Drayage is a patchwork of small operators, while freight forwarding has some global giants with robust IT systems. Most drayage carriers lack the tech to compete, relying on phone calls and emails.

The Drayage Dumpster Fire

Because drayage sits at the center of many important handoffs, it’s a logistical nightmare.

Port Congestion: Drivers face 85-minute average wait times at terminals, burning fuel and hours. Missing a port appointment slot can delay a load by a day, racking up demurrage fees or detention pay.

Chassis Shortages: Only 700K chassis serve 35M annual container moves. If a driver shows up and there’s no chassis? Tough luck, the job’s stalled.

Manual Everything: Dispatchers coordinate via phone calls, email threads, and spreadsheets. Most Transportation Management Systems (TMS) aren’t built for drayage’s quirks, like port integration or dual transactions (drop-off and pick-up in one trip).

Regulations: Ports like LA enforce strict emissions rules or programs like PierPass, which slaps fees on peak-hour moves. California’s AB5 law shook up the driver model, reclassifying many independents and shrinking the workforce.

Driver Shortages: Drayage drivers earn less per day due to low mileage and unpaid wait times, making port trucking a tough sell in a tight labor market.

These pain points create a vicious cycle of inefficiency, costing carriers time and money.

AI Opportunities

Drayage’s problems – communication breakdowns, coordination chaos, and operational fragility – are problems that AI can address. Some ideas:

1. Back‑Office Workflow Automation

AI agents integrate directly with a carrier’s email inbox to automate RFQ extraction, quote generation, rate negotiation, dispatch scheduling, invoicing, and payments – compressing hours of manual work into seconds.

They can also handle:

Chassis billing reconciliation – a persistent headache due to mismatched charges

Per diem dispute management – flagging customer-caused delays before penalties escalate

Container tracking – monitoring dwell time and alerting carriers to at-risk loads

2. Predictive Scheduling & Route Optimization

ML models forecast:

Port congestion

Peak traffic windows

Using this, the system recommends optimal pickup/drop‑off times and load sequencing based on a carrier’s historical “turns per day” – maximizing daily revenue instead of using simplistic per-mile logic.

3. Platform Extensions & Value‑Added Services

Beyond core operations, AI can:

Automate invoicing to factoring partners for faster cash flow

Send compliance alerts (e.g., TWIC/SCAC expirations)

Transcribe driver voice notes into structured job logs for dispatch and billing systems (similar to what I wrote about for the field service trade here).

Skip the Small Fry

Selling to tiny owner-operators one by one is a slog. Instead there’s an opportunity to target freight forwarders or large importers/exporters directly. Forwarders rely on reliable drayage to deliver end-to-end service, and they’re incentivized to adopt tech that makes their drayage vendors more efficient.

Drayage as a Wedge, Not a Destination

Given drayage’s relatively limited market size, I see it less as an end destination and more as a strategic wedge. The sector is operationally broken in ways that are ripe for startups to address – offering fast paths to measurable value. Most inefficiencies are clear operational gaps: disjointed communication, manual workflows, and suboptimal routing.

A platform that solves those pain points can quickly build credibility, and from there, expand into adjacent logistics services where the real scale lives. Win drayage, and you earn the trust, data, and distribution to tackle the broader freight ecosystem.

It's trucking and not drayage, but you should check out AIFleet.

https://aifleet.com/about

Drayage is the part of freight that everyone steers clear of because dealing with customs is a nightmare