The Freight Market Has Bottomed Out. Now What?

The Freight Recession and the Role of AI in the Industry’s Recovery

Every cycle in freight feels both familiar and surprising. Rates surge, networks expand. Then demand softens, capacity floods the market, and pricing craters. But each downturn reveals something about how this industry reacts, and how it might one day learn to predict instead of react.

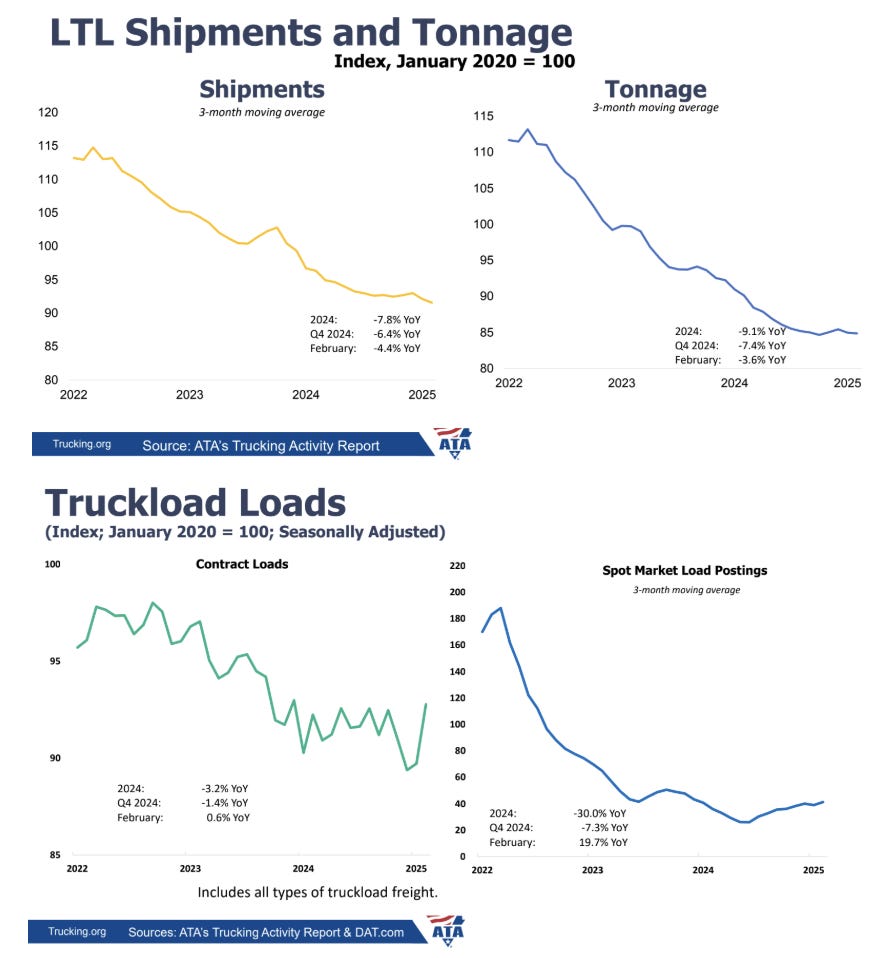

At this year’s Inland25 conference, the consensus across carriers, brokers, and shippers was that the market has hit bottom. Across truckload, intermodal, and cross-border, pricing has fallen to unsustainably low levels, and few expect further decline. The broader freight industry is now in its third year of contraction, the longest and deepest in more than two decades. Volumes are weak, rates are flat, and operating costs are rising, from insurance and wages to fuel and compliance. The result is a squeeze that touches every node of the supply chain.

As the market has bottomed out, there’s an opportunity to reimagine how freight companies operate.

The Freight Recession

While freight rates are low, insurance premiums are up 6% YoY, driver wages continue to climb, and compliance costs (spanning fraud prevention and Federal Motor Carrier Safety Administration (FMCSA) regulations) add new friction. This tough environment leaves many operators in what someone at Inland25 described to me as a “quiet squeeze” – stuck at the bottom, with little leverage. Carriers can only absorb these rising costs for so long; when volumes tick up, even modestly, they’ll need to raise rates to restore margins, meaning the eventual rebound could feel sharper than expected.

Overcapacity compounds the issue. Too many trucks and containers are chasing too little freight, a legacy of pandemic-era buildout. Structural shifts also play a role. Amazon’s decade-long push into logistics created a parallel freight network, flooding certain lanes with its own capacity and driving rates below sustainable levels. Even in truckload and regional freight, one carrier’s willingness to undercut prices keeps the floor low for everyone.

Trade policy uncertainty is another headwind. Tariffs (both those enacted in recent years and new ones now proposed) have injected a layer of unpredictability into global freight planning. When shippers can’t forecast the landed cost of goods or the stability of trade lanes, they delay orders, hold less inventory, and rethink sourcing strategies. The effect isn’t just lower volume but erratic demand, with freight flows swinging in response to policy headlines rather than economic fundamentals. For carriers and brokers, that uncertainty makes network planning harder, asset utilization lower, and pricing discipline nearly impossible.

So when does the turn come? Spot rates typically move first, reflecting real-time shifts in demand. Based on historical cycles, analysts don’t expect meaningful upward movement until at least Q2/26. C.H. Robinson projects only ~2% YoY growth in spot rates next year, a small number, but one that could signal the cycle’s turn.

Capacity exits will also be uneven. When large carriers shutter terminals or small fleets go under, those assets vanish locally even if national supply looks steady. These regional imbalances will cause the rebound to play out in fits and starts, with some modest local price increases long before the broader market recovers.

The Role of AI

The challenge for carriers is to survive until the rebound without burning capital. For shippers, it’s preparing for the cost pass-throughs once it hits. This is where AI can play a transformational role, both in day-to-day operational efficiency and strategic intelligence.

Day-to-Day Operational Efficiency

Freight brokerages and carriers run on thin margins and employ large back-office teams to maintain service levels. For example, track-and-trace teams spend their days calling drivers to confirm locations and update shippers, even when telematics data exists. In parallel, operations teams are manually reconciling documents: entering pickup numbers, validating lumper receipts, matching invoices to loads, or flagging accessorial charges for approval. Each of these steps is critical to maintaining cash flow and service reliability, but collectively they represent many thousands of human hours spent on low-value, high-volume administrative work.

AI can automate these manual workflows by ingesting ELD and GPS data, inferring anomalies, flagging delays, and generating automated status updates. Computer vision models can read lumper receipts and bills of lading directly from driver uploads; language models can cross-check those documents against rate confirmations or TMS entries in real time. The result is fewer touches per load, faster invoicing cycles, and dramatically lower operating costs.

These efficiencies can lead to better margins during the good times and breathing room during down cycles.

Strategic Intelligence

If day-to-day operational efficiency is about expanding margin, strategic intelligence is about anticipating market shifts.

AI models can detect regional demand shifts before they appear in spot data, pulling from signals like port throughput, tariff filings, customs declarations, housing starts, or even building permits that hint at future industrial and retail activity. A model trained on these indicators could anticipate where freight demand is likely to tighten or loosen weeks (or more) before it’s reflected in rates. Carriers could redeploy assets or exit underperforming lanes early. Shippers, meanwhile, could use similar intelligence to dynamically rebalance their freight mix across truckload, intermodal, and cross-border modes, adjusting allocations as relative prices and capacity conditions shift.

The result is a network that plans forward rather than reacts late, turning what’s long been an instinct-driven business into one governed by proactive, data-driven decisioning.

Proactive Action Systems

Historically, freight technology has been retrospective: dashboards that describe what happened. The next generation will be proactive: systems that surface signals and act on them automatically, adjusting lane agreements, rerouting freight, or alerting sales teams when margin erosion is likely. These same systems will also close the loop operationally (issuing updated rate quotes, triggering shipment re-plans, or reconciling documentation without human intervention). Instead of a dozen disconnected tools and manual workflows, AI will unify visibility and provide the basis for fast, intelligent decision-making.

Over time, better forecasting and faster feedback loops will undoubtedly smooth the extremes of future cycles. When carriers can see demand softening before it crashes, or shippers can model the true impact of rate hikes before pulling back, the collective overreactions that define freight’s booms and busts may start to soften. AI won’t eliminate volatility as it’s too deeply tied to macro demand; but it can shorten the lag between signal and response, helping the industry move from reactive swings to more measured adjustments.